{kind=link}

There are a few reasons why this strategy is attractive to currency traders.

Firstly it can, under certain conditions give a predictable outcome in terms of profits. It’s not a sure bet, but it’s about as close as you can get.

Secondly it doesn’t rely on an ability to predict absolute market direction. This is useful given the dynamic and volatile nature of foreign exchange.

With deep enough pockets, it can work when your trade picking skills are no better than chance. Though it does have a far better outcome, and less drawdown, the more skillful you are at predicting the market ahead.

And thirdly, currencies tend to trade in ranges over long periods – so the same levels are revisited over many times. As with grid trading, that behavior suits this strategy.

Martingale is a cost-averaging strategy. It does this by “doubling exposure” on losing trades. This results in lowering of your average entry price.

The important thing to know about Martingale is that it doesn’t increase your odds of winning. Your long-term expected return is still exactly the same. It’s governed by your success in picking winning trades and the right market. You can’t escape from that.

What the strategy does do is delay losses. Under the right conditions, losses can be delayed by so much that it seems a sure thing.

What Is Martingale And How Does It Works

In a nutshell: Martingale is a cost-averaging strategy.

It does this by “doubling exposure” on losing trades. This results in lowering of your average entry price. The idea is that you just go on doubling your trade size until eventually fate throws you up one single winning trade. At that point, due to the doubling effect, you can exit with a profit.

A Simple Win-Lose Game

This simple martingale strategy example shows this basic idea. Imagine a trading game with a 50:50 chance of winning verses losing.

| Stake | Outcome | Profit/Loss | Running Balance |

| $1 | Win | $1 | $1 |

| $1 | Win | $1 | $2 |

| $1 | Lose | -$1 | $1 |

| $2 | Lose | -$2 | -$1 |

| $4 | Lose | -$4 | -$5 |

| $8 | Win | $8 | $3 |

Table 1: Simple betting example.

I place a trade with a $1 stake. On each win, I keep the stake the same at $1. If I lose, I double my stake amount each time. Gamblers call this doubling-down.

If the odds are fair, eventually the outcome will be in my favor. And since I’ve been doubling my stake each time, when this happens the win recovers all of the previous losses plus the original stake.

This is thanks to the double-down effect. Winning bets always result in a profit. This holds true because of the mathematical fact that 2n = ∑ 2n-1 +1. That means the string of consecutive losses is recovered by the last winning trade.

If you’re interested in experimenting with the toy system, here is a simple betting game spreadsheet:

A Basic Trading System

In real trading there isn’t a strict binary outcome. A trade can close with a certain profit or loss. But this doesn’t change the basic the strategy. You just define a fixed movement of the underlying price as your take profit, and stop loss levels.

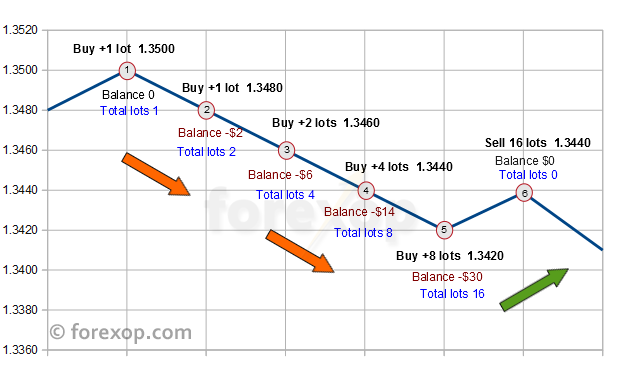

The following case shows this in action. I’ve set my take profit and stop loss at 20 pips.

| Rate | Order | Lots (micro) | Entry | Avg. Entry | Abs. Drop (pips) | Break Even (pips) | Balance $ |

| 1.3500 | Buy | 1 | 1.3500 | 1.3500 | 0.0 | 0.00 | $0 |

| 1.3480 | Buy | 2 | 1.3480 | 1.3490 | -20.0 | 10.00 | -$2 |

| 1.3460 | Buy | 4 | 1.3460 | 1.3475 | -40.0 | 15.00 | -$6 |

| 1.3440 | Buy | 8 | 1.3440 | 1.3458 | -60.0 | 17.50 | -$14 |

| 1.3420 | Buy | 16 | 1.3420 | 1.3439 | -80.0 | 18.75 | -$30 |

| 1.3439 | Sell | 16 | 1.3439 | 1.3439 | -61.2 | 0.00 | $0 |

Table 2: Averaging down trade entry levels in falling market.

I start with a buy to open order of 1 lot at 1.3500. The rate then moves against me to 1.3480 giving a loss of 20 pips. It reaches my virtual stop loss.

It’s a virtual stop loss because in real trading there would be no point in closing the position, and opening a new one for twice the size. I keep my existing one open on each leg and add a new trade order to double the size.

Martingale

Complete Course

A complete course for anyone using a Martingale system or planning on building their own trading strategy from scratch. It's written from a trader's perspective with explanation by example. Our strategies are used by some of the top signal providers and traders

So at 1.3480 I double my trade size by adding 1 more lot. This gives me an average entry rate of 1.3490. My loss is the same, but now I only need a retracement of +10 pips to break even rather than 20 pips as before.

The act of “averaging down” means you double your trade size. But you also reduce the relative amount required to re-coup the losses. This is shown by the “break even” column in Table 2.

The break-even approaches a constant value as you average down with more trades. This constant value gets ever closer to your stop loss. This means you can catch a “falling market” very quickly and re-coup losses – even when there’s only a small retracement.

Standard Martingale will always recover in exactly one stop distance, regardless of how far the market has moved against the position. (see Figure 1).

{kind=link}

At trade #5, my average entry rate is now 1.3439. When the rate then moves upwards to 1.3439, it reaches my break-even.

I can close the system of trades once the rate is at or above that break even level. My first four trades close at a loss. But this is covered exactly by the profit on the last trade in the sequence.

The final P&L of the closed trades looks like this:

| Order | Lots | Entry | P&L |

| Buy 1 | 1 | 1.3500 | -$6.12 |

| Buy 2 | 1 | 1.3480 | -$4.12 |

| Buy 3 | 2 | 1.3460 | -$4.25 |

| Buy 4 | 4 | 1.3440 | -0.50 |

| Buy 5 | 8 | 1.3420 | $15.00 |

| Totals | 16 | $0.00 |

Table 3: Losses from previous trades are offset by the final winning trade.

Does the Martingale strategy work?

In a pure Martingale system no complete sequence of trades ever loses. If the price moves against you, you simply double the size of the trade.

But such a system can’t exist in the real world because it means having an unlimited money supply and an unlimited amount of time. Neither of which are achievable.

In a real trading system, you need to set a limit for the drawdown of the entire system. Once you pass your drawdown limit, the trade sequence is closed at a loss. The cycle then starts again.

When you restrict the ability to drawdown, you’re no longer using a pure Martingale system. And in doing so you’re using an approximation that will always have a failure point.

Doubling-down verses Probability of Loss

The dilemma is that the greater your drawdown limit, the lower your probability of making a loss – but the bigger that loss will be. This is the Taleb dilemma.

The more trades you do, the more likely it is that those extreme odds will “come up” – and a long string of losses will wipe you out.

In Martingale the trade exposure on a losing sequence increases exponentially. That means in a sequence of N losing trades, your risk exposure increases as 2N-1. So if you’re forced to exit prematurely, the losses can be truly catastrophic.

On the other hand, the profit from winning trades only increases linearly. It’s proportional to half the profit per trade multiplied by total number of trades.

{kind=link}

Winning trades always create a profit in this strategy. So if you pick winners 50% of the time (no better than chance) your total expected return from the winning trades would be:

E ≈ ½ N x B

Where N is the number of “trades” and B is the amount profited on each trade.

But your big one off losing trades will set this back to zero. For example, if your limit is 10 double-down legs, your biggest trade is 1024. You would only lose this amount if you had 11 losing trades in a row. The probability of that is (1/2)11. That means, every 2048 trades, you’d expect to lose once.

So after 2048 trades:

- Your expected winnings are (1/2) x 211 x 1=1024

- Your expected one off loss is -1024

- Your net profit is 0

So your odds always remain 50:50 within a real system. That’s assuming your trade picking is no better than chance.

Your risk-reward is also balanced at 1:1. But unlike most other strategies, in Martingale your losses will be seldom but very large. So managing that can be difficult, especially if you’re unlucky and it happens before you’ve had a chance to accumulate any profit!

The point to take from all of this is that Martingale can’t improve your odds of winning. It just postpones your losses. See Table 4.

| #Trades | Expected winnings | Expected loss (1 off event) | Net (average) |

| 1 | 0.5 | -0.5 | 0 |

| 2 | 1 | -1 | 0 |

| 4 | 2 | -2 | 0 |

| … | … | … | … |

| 512 | 256 | -256 | 0 |

| … | … | … | … |

Table 4: Your winning odds aren’t improved by Martingale. Your net return is still zero.

Those people who’re trend followers at heart often believe it’s better to use a reverse Martingale. The anti-Martingale or reverse Martingale tries to do the exact opposite of what’s described above. Basically it is a trend following strategy that double up on wins, and cut losses quickly.

Stay Away from “Trending” Currencies

The best opportunities for the strategy in my experience come about from range trading. And by keeping your trade sizes very small in proportion to your capital, that is using very low leverage. That way, you have more scope to withstand the higher trade multiples that occur in drawdown.

The most effective use of Martingale in my experience is as a yield enhancer.

There are of course many other views however. Some people suggest using Martingale combined with positive carry trades. What that means is trading pairs with big interest rate differentials. For example, using the strategy of long-only trades on AUD/JPY.

Price Action Trading

Definitive Guide

Price action trading with candlesticks gives a straightforward explanation of the subject by example. It includes data insights showing the performance of each candlestick strategy by market, and timeframe.

The idea is that positive rollover credits accumulate because of the large open trade volumes.

However there are problems with this approach. The risks are that currency pairs with carry opportunities often follow strong trends. These instruments often see steep corrective periods as carry positions are unwound (reverse carry positioning).

This can happen suddenly and without warning. For example if there are unexpected changes in the interest rate cycle, or if there’s a sudden change in risk appetite in which case funds tend to move away from high-yielding currencies very quickly (read more about carry trading.)

Analysis shows that over the long term, Martingale works very poorly in trending markets (see return chart – opens in new window).

It’s also worth keeping in mind many brokers subject carry interest to a significant spread – which makes all but the highest yielding carry trades unprofitable. Some retail brokers don’t even credit positive rollovers at all.

Lastly, the low yields mean your trade sizes need to be big in proportion to capital for carry interest to make any difference to the outcome. As the above example shows, this is too risky with Martingale.

The strategy better suited to trending is Martingale in reverse.

Using Martingale as a Yield Enhancement

Martingale shouldn’t be used as a main trading strategy. This is because for it to work properly, you need to have a big drawdown limit relative to your trade sizes. If you’re using a large pool of your trading capital, there’s a very real risk of “going broke” on one of the downswings.

A better use of Martingale in my experience is as a yield enhancer with low leverage.

The least risky trading opportunities for this are pairs trading in tight ranges.

Volatility tools can be used to check the current market conditions as well as trending. The best pairs are ones that tend to have long range bound periods that the strategy thrives in.

Martingale can survive trends but only where there’s sufficient pullback. This is why you have to watch out for break-outs of significant new trends – watch out especially around key support/resistance levels.

Trading pairs that have strong trending behavior like Yen crosses or commodity currencies can be very risky.

The image below shows an example yield enhancer strategy covering a period of 3-months producing a 9% return.

{kind=link}

The low leverage here allows drawdown to be kept within manageable limits.

Calculate Your Drawdown Limit

A good place to start is to decide the maximum open lots you’re able to risk. From this, you can work out the other parameters. To keep things simple, I’ll use powers of 2.

The maximum lots will set the number of stop levels that can be passed before the position is closed. In other words it’s the number of times the strategy will “double-down”. So for example, if your maximum total holding is 256 lots, this will allow doubling-down 8 times – or 8 legs. The relationship is:

max lots = 2Legs

If you close the entire position at the nth stop level, your maximum loss would be:

max loss = (2n-1) x s

Here s is the stop distance in pips at which you double the position size. So, with 256 lots (micro lots), and a stop loss of 40 pips, closing at the 8th stop level would give a maximum loss of 10,200 pips. Closing at the 9th stop level would give a loss of 20,440 pips.

Tip Work out the average number of trades you can handle before a loss – use the formula 2Legs+1. So in the example here that’s just 29, or 512 trades. So after 512 trades, you’d expect to have a string of 9 losers given even odds. This would break your system.

You can use the lot calculator in the Excel workbook to try out different trade sizes and settings.

The best way to deal with drawdown is to use a ratchet system. As you make profits, you should incrementally increase your lots and drawdown limit. For example, see the table below.

| Iteration # | Realized equity | Drawdown allowed | Profit |

| 1 | $1,000 | $1,000 | $25 |

| 2 | $1,025 | $1,025 | $5 |

| 3 | $1,030 | $1,030 | -$10 |

| 4 | $1,020 | $1,020 | $5 |

| 5 | $1,025 | $1,025 | $20 |

Table 5: Ratcheting up the drawdown limit as profits are realized.

This ratchet is demonstrated in the trading spreadsheet. You just need to set your drawdown limit as a percentage of realized equity.

Warning Since Martingale trading is inherently risky your capital at risk shouldn’t ever exceed 5% of your account equity. See the money management section for more details.

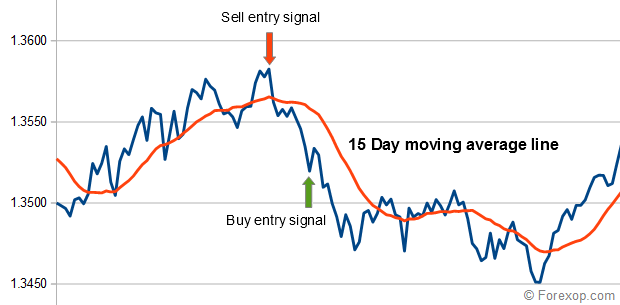

Decide On an Entry Signal

The system still needs to be triggered some how to start buying or selling at some point. Any effective buy/sell signal can be used but the better it is, the better the strategy will work, and the lower the drawdown.

In the examples here I’m using a simple moving average. When the rate moves a certain distance above the moving average line, I place a sell order. When it moves below the moving average line, I place a buy order. This system is trading false break-outs, also known as “fading”.

In my system, I’m using the 15 point moving average (MA) as my entry signal. The length of moving average you choose will vary depending on your particular trading time frame and general market conditions.

This is a very simple, and easily implemented triggering system. There are more sophisticated methods you could try out. For example, divergences, using the Bollinger channel, other moving averages or any technical indicator.

{kind=link}

Strong breakout moves can cause the system to reach the maximum loss level. So trading near to key support/resistance areas, in volatility squeezes, and before data releases should be minimized as far as possible.

For more details on trading setups and choosing markets see the Martingale eBook.

Set the Take Profit and Stop Loss

The next two points to think about are

- When to double-down – this is your virtual stop loss

- When to close – your “take profit level”

When to double-down – this is a key parameter in the system. The “virtual” stop loss means you assume at that point the trade has gone against you. It’s a loser. So you double your lots.

Choose too small a value and you’ll be opening too many trades. Too big a value and it impedes the whole strategy.

The value you choose for your stops and take profits should ultimately depend on the time-frame you’re trading and the volatility. Lower volatility generally means you can use a smaller stop loss. I find a value of between 20 and 70 pips is good for most situations.

When to close Trades in Martingale should only be closed when the “entire system” is in profit. That is, when the net profit on the open trades is at least positive. As with grid trading, with Martingale you need to be consistent and treat the set of trades as a group, not independently.

A smaller take profit value, usually around 10-50 pips, often works best in this setup.

There are a couple of reasons for this.

- A smaller take profit level has a higher probability of being reached sooner so you can close while the system is profitable.

- The profit gets compounded because the lots traded increase exponentially. So a smaller value can still be effective.

Using a smaller take profit doesn’t alter your risk reward. Although the gains are lower, the nearer win-threshold improves your overall trade win-ratio.

Divergence Trading Pack

Chart Indicator

Pack of indicators for divergence traders. Includes a technical divergence tool, an indicator for analyzing divergence between asset types, and a stop/profit advisor.

Simulations

The table below shows my results from 10 runs of the trading system. Each run can execute up to 200 simulated trades. I started with a balance of $1,000 and drawdown limit 100% of that amount. The drawdown limit is automatically ratcheted up or down each time the realized P&L changes.

| Run # | Profit | Run. Balance | Drawdown limit | Worst drawdown | Return |

| 1 | $22 | $1022 | $1,000 | -$5.25 | 2.2% |

| 2 | $36 | $1,058 | $1022 | -$38.43 | 3.4% |

| 3 | $37 | $1,095 | $1,058 | -$31.50 | 3.4% |

| 4 | $147 | $1,242 | $1,095 | -$346.86 | 11.8% |

| 5 | $141 | $1,383 | $1,242 | -$153.31 | 10.2% |

| 6 | $205 | $1,588 | $1,383 | -$377.81 | 12.9% |

| 7 | $46 | $1,634 | $1,588 | -$63.44 | 2.8% |

| 8 | $101 | $1,735 | $1,588 | -$87.12 | 5.8% |

| 9 | $35 | $1,770 | $1,588 | -$12.70 | 2.0% |

| 10 | $26 | $1,796 | $1,588 | -$10.20 | 1.4% |

Table 6: Simulation results from the spreadsheet.

My final balance was $1,796 which gives an overall return of 79.6% on the initial starting amount.

The chart below shows a typical pattern of incremental profits. The orange line shows the relatively steep drawdown phases.

{kind=link}

[bctt tweet=”Martingale doesn’t increase your odds of winning. It just delays losses – for a long time if you’re lucky.” nofollow=”yes”]

The spreadsheet is available for you to try this out for yourself. It is provided for your reference only. Please be aware that use of the strategy on a live account is at your own risk.

Pros and Cons of Martingale

Why Use It:

- It has a well defined set of trading rules that can be easily followed or programmed as an Expert Advisor.

- It has a statistically computable outcome with respect to profits and drawdowns.

- When applied correctly it can achieve an incremental profit stream.

- You don’t need to be able to predict the market direction.

Why Avoid It:

- Averaging down is a strategy of avoiding losses rather than seeking profits.

- Martingale doesn’t increase your odds of winning. It just delays losses – for a long time if you’re lucky.

- It relies on assumptions about random market behavior which are not always valid. Markets do behave irrationally.

- The risk exposure increases exponentially, while the profits increase linearly.

- It can potentially run up catastrophic losses in practice because nobody has an unlimited amount of money.

- The risk v.s reward is balanced, but because the loss comes in one big hit it can be unacceptable.

For more information on Martingale see our eBook.

Contact me i have updated Martingale ..

Do not take any Bonus offer from your broker or your manager, do not allow your broker manager trade on your behalf. That is how they manipulate traders funds. If you need assistance with retrieving your lost fund from your broker or Your account has been manipulated by your broker manager or maybe you are having challenges with withdrawals due to your account been manipulated. Kindly get in touch with me and I will guide you on simple and effective steps to take in getting your entire fund back.

If you are doing Martingale as a limited automatic system, it might not cause huge harm, but if you are doing it as a way to prevent loss, you might want to reconsider what’s going on in your mind, Things related to narcissism. cause you already have negative profit for one or more of your positions, opening another position to cover it up?! may be you are as what i’ve faced in myself running from losing. Instead by paying for a small loss for a position you can take full profit of your another position and market is not always random and unpredictable. Elliot waves and fibonacci comes handy in recognizing the trend.

If the system is set up correctly, everything works well. It is clear that the option is possible that sooner or later everything will be at 0. But when the balance is large, the chance decreases almost to 0.

How do you handle trend change from range? There were times when I open a trade at support or resistance but the price broke out and never came back and all my doubles becomes counter trend trades, hoping for a pull back to cover all losts.

I am working on Martingale strategy and its too risky, so to reduced Drawdown I have to add winning positions in with Losing positions to Limit drawdown to possible low I am unable to set such Lot of trades so that T.Ps are at the same Price so that At any point point market kick back both my losing side T.P and wining side T.P will hit can you help me on this ?

contact me i have a good strategy with martingale

adil contact me

Hi Adil

Please send me the strategy,i wanna try it,have been losing

Regards

Paula

hello beautiful traders. , I am very happy with this article, many people believe martingale strategy don’t work, well I used to, but then I realised nothing is impossible, I havebeen trading for over four years, and my only strategy has been martingale, I have learnt and developed my myself better using this strategy. I am an account manager and I have clients invested thousands of dollars, and I manage their funds using this strategy, the secret about this strategy is ample deposit, and tight take profit, I started my first year managing my own account of $170 back in 2014 and turn it into $1200+ in seven months, and guess what it wiped out the 8th month, then I went back to see what happened, the condition that lead to this disaster and what I was doing wrong and how to get better, with my strategy I only trade just one single pair, now I trade in millions using martingale, double my investment in 2years is my strategy, and I can go up to 500pips in trend without reaching half of my deposit, I can place up to 35trades at a time using martingale and I will be doing just fine, I use this strategy only m1 chart 24/7 without fear, if you want to start out with a martingale system focus on the risk and not the profit. when you make profits, you protect them and not expose to more risk, I use take profit as little as 2pips. the quick you take your profit the lesser your risk percent, I use a simple hedging buy and sell martingale system with very good money management. If you are curious about how I do my thing. I will be very happy to share with you. thank you

Hi i would be interested in learning how you trade martingale 🙂

Let me take you up on your offer. Can you share with me? Thanks.

PLEASE SHOW ME

hello trader, would you still be willing to share?

If by chance you decide to share your strategy with us, just remember there’s a long queue of us itching to learn about your concept. I basically trade the same way of using a hedged martingale system but I’m yearning to improve on it and reduce the risks. Thanks

hey bro! i am curious do you have telegram ?

“I use this strategy only m1 chart 24/7”

For martingale why you r using chart. So you open trade based on signal right. Then why you do both buy and sell

I am interested in your martingale strategy in forex..kindly contact me how to start..thanks

Hi I am interested please share your contact details

Hi can you tell me your way please? i am trying to develop a sytem with Mgale that works.

There is a way to achieve infinity money. Infinity doesn’t have to be big number but can be infinitely small. In other words, 100 percent of your portfolio divided by a large number close to infinity.

I thought I am the only one traded with this method because I figure the whole trading method using mathematical, psychological and logical thinking. Until today I came across this method actually has a name on it.

I was a veteran ex stock retail trader by practise. Forex trading is entirely new to me. I started Forex Trading since Nov17. There are few things in common. Number, Charts and Percentage.

I did not read your ebook about martingale because I usually do not copy others trading method.

My initial experiments on demo account was to rapidly gain % and it ends up with a margin call which I had no clue how that works. I figured that out later on. Second attempt was to burn my demo account as quickly as possible by using double down method. It works exactly the same as you describe above, it got margin call after 74% gain in 3 days.

Im on the third demo account with fine tuning martingale method. Im up 124% in 23 consecutive winning days and 100% winning trade. I think I am lucky on it. I only trade EU pair. The last trade happens to hold 4days because of losing trade, and unable to take profit during g sleep hour. it end up breaking my buy price with a gain in daytimd. As I am still in the process of learning.

From Mathematical approach, what I did was gap between entry price need to be proportional to your lot size. It can’t be linear like what you mentioned in table 3. Example, buy 1.2230 1lot. Buy 1.2200 2lot. Buy 1.2140 4lot instead of buy 1.2170 etc or base on whatever indicator that trigger another buy call. Secondly, Instead of waiting the whole set of trade to be profitable. Take profit once the newest trade start to trend to your direction. It is to cash out and free up the capital, so when it reverse your trend again, we can reenter with 4lot instead of 8lot. Greatly reduce risk involved.

From logical approach, I don’t treat it as double down. I rather think it as spread betting, I would actually thinking I need to place 15 lot (up to whatever spread or double down you want to call it), so I am actually be delighted when it go against my trend, because I could buy it at cheaper price.

From psychological approach, making mistake is part of the trading, it should be allowed in our system with a backup strategic, hence martingale.

Anyway, I am just a 3months old novice trader. You might not need to take my message seriously.

Thanks

Ted

Ted. How did it go for you. I like your ideas a lot.

We should stay away from Martingale as it is very dangerous.Think of the 2*spreads you have to pay on every doubling trade+risk of spending all amount in chain trading

Thank you for your explanation and effort

is it possible to program an EA to use martingale strategy in a ranging or non trending market and stop it

if the market trends like cover a large predefined number of pips (eg 300 pips) in certain direction and then

uses Martingale in reverse

the ea should have a trend sensor according to result it changes the strategy.

do you think it will work? do you think it can be done?

The trading system is a lot more complicated then I thought. I’m glad you explained it in a simple and brief way with charts and graphs. A lot of financial advisors use tvalue. Martingale sounds a great way to become more knowledgeable in the trading system.

How a about hedging martiangle with price action..exam:candlestick or S nR

Martingale can work really well in narrow range situations like in forex like when a pair remains within a 400 or 500 pip range for a good time. As the other comment said if there is a predictable rebounding the opposite way that is the ideal time to use it. Then the strategy has to be smart enough to predict when the rebounds happen and in what size. The amount of the stake can depend on how likely it is for a market run-off one way or the other, but if the range is intact martingale should still recover with decent profit.

How can I determine porportionate lot sizes by estimating the retracement size. Example,

EURUSD has gone up by 200 pips and I want to have proportionate lot sizes so that I can

recover my 200 pips drawdown. My estimate is that retracement will be of only 10% or 20

pips but I want to recover 200 pips by 5 lots and not by one constant lot based on my margin balance.

Is there any formula to work backwards and determine proportionate lots for such a situation?

Thank you

I’m not sure I understand your question because if the order is already placed what good is it then knowing the size you need to recover? The recovery size you need would depend on where the other orders were placed and what the sizes were – you will have to do a manual calculation. Starting with a new set of orders, if you multiply the size by 6 (instead of 2) from the start that will recover in 20% of your stop distance. But you can’t change that multiple once you have open positions, the other calculations won’t work. Hope that helps.

Great article please I had like to know what are your trading numbers while using the martingale strategy

The system I was using would make low single digit returns. Obviously you can leverage that up to anything you want but it comes with more risk.

I’ve been testing for a couple of years on the pair EURUSD with hourly data from 2005 to 2016.

My goal is to achieve a 20-25% on the first bet. If I have to double-down then I change my goal to just 1% because I realized that there are a few days just 4 or 5 in 10 years that are horrible if I keep on my 20% goal. So I assume that if the market is against me then I want to quit as soon as possible squeezing my potential earnings.

If leverage increases then :

• Slight oscillations on price easily moves me to the expected 20%. On a 200 leverage, if price moves only 0,1% in my direction I win. So even if the trend is against me, sometimes during an hour, the price oscillates on my side.

• Chances to bankruptcy are also higher. This is true. That’s why as soon as I double-down, I reduce the goal to just 1% from 20%.

• Tests show me that using such strategy I reduce half of the bankruptcy days if I double leverage.

One thing I think It could be interesting is to work more on the winning bets. I mean, now I close my bets as soon they achieve the 20% goal but working on leverage 100 or 200 and being in the right trend, it is easy to make a 100% or 200% profit. Any Ideas or known strategies about it are welcome.

Salutacions

Hi Steve,

Is this the Martingale ea in the downloads section?

Thanks

Russ

Hi Steve,

Thank you for sharing this wonderful article. So you are talking about Dollar Cost Averaging system above. But I guess the maximum drawndown is not correct. Is the drawdown of the last trade or the whole cycle ?

Thank you

The limit is for the whole cycle. The TP is not a take profit in the regular sense. It’s the point which the system doubles down so the trades “above it” remain open.

With the example I gave above this is how the whole cycle would look like just before closing:

Position Size Limit Drawdown

1 1 360 360

2 1 360 360

3 2 280 560

4 4 240 960

5 8 200 1600

6 16 160 2560

7 32 120 3840

8 64 80 5120

9 128 40 5120

Giving an effective total of 20480 pips ($2048 dollar amount if using micro account) which is where formula below comes from:

Max lots x ( 2 x Stop Loss ) x Lot size = 256 x (2 x 40) x 0.1

Hi Steve,

I guess there is a typo. In your formula for maximum drawdown, you are assuming 20 pips TP, which becomes 40 pips when it gets multiplied with 1 or your are assuming 40 pips ? Secondly, the term maximum lot is the maximum lot size of 8th trade or total lots of 9 trades (1 original trade + 8 legs)?

Thank you

Please see explanation above.

Hi,

Have you heard about Staged MG? Sometimes called also Multi Phased MG?

It means that each time the market moves you take just a portion of the overall req. trade, and you

continue only if the market goes in the “right” direction.

What do you think about this strategy?

Is it safer than regular MG?

BTW, can I have your email please for a personal question?

TIA

I’ve seen variations like this before and some others.

In fact the Excel sim spreadsheet – https://forexop.com/?wpdmact=4508 – we have lets you do something like this.

It lets you use a different compounding factor other than the standard (2). So instead of 2x for example that you have with standard MG you can use 1.5 X or 1.2 X or any other factor.

The interesting thing is you say when the “market moves in the right direction”. That makes me think what you are talking about is more of a hybrid strategy because a standard Martingale system doubles down on losers – namely it’s increasing exposure as the market moves against you not the other way around. Therefore this sounds more like a reverse-martingale strategy.

Very interesting article but I still don’t understand what you mean by:

“The best way to deal with drawdown is to use a ratchet system. So as you make profits, you should incrementally increase your lots and drawdown limit.”

Could you explain what you are doing here? Looking at you table you are increasing the drawdown limit based on profits made previously, but you stop increasing the limit at the 7th run.

Thanks

This ratchet approach basically means giving the system more capital to play with when (if) profits are made. So in the early runs the number of times the system will double down is less and hence the drawdown limit is lower. But with each profit this drawdown limit is incremented in proportion to the profits – so it will take more risk. I use this as a way of locking in profits so that the system is able to “play with money” that it makes so to speak. In the example the reason it stops at line 7 is just because in practice the drawdown occurs in steps (because of the doubling down). I would have to check the simulation in detail – but it would seem that it’s hit a step here and the profit needs to increase by more to take it to the next one.

Hi Steve,

Very good article, I read it many times and learned a lot. Thank you.

Currently I’m working on martingale trading system with implemented hedging function to limit drawdown.

My question would be how to chose currencies to trade Martingale? You suggested to stay away from trending markets. What indicators and setups could help identify most suitable pairs to trade?

You are welcome. To choose currencies I would firstly check the fundamentals: For example you wouldn’t want to risk trading currencies where there’s an expectation of widely diverging monetary policy. This was (is) the case with EURUSD. EURGBP and EURCHF were good candidates in the past but not at the moment for several reasons. EURCHF can’t really be considered fully floating because of central bank intervention while EURGBP has been trending for some time in part because of the reasons mentioned above. I’ve also used a ranging indicator as this can help identify the most productive periods, namely volatile but predominantly sideways price movement.

Hi Steve, how much balance you should have to run this strategy? 2k? 3k?

Balance is relative to your lot sizing. If you can find a broker that will do fractional sizing (< 0.01 say), that gives you the most flexibility to scale the system as you need it. With 2k or 3k the ideal would be nano lots.

Hi, Steve

Thanks for the wonderful explanation. I suspect my fund manager uses martingale. Can you tell by the looks of it?

Kindky see image:

https://www.dropbox.com/s/3djgjbibngr29mq/martingale.jpg?dl=0

Thank you!

Could’t tell a great deal from this image as it doesn’t show any returns.

Hi, intyeresting post.

Are you still running martingale on USD/EUR?

How it performed during 2015?

I’ve been testing a simple strategy based on martingale but during 2015 it’s been horrible!!

My strategy better performs with high leverage of 100 or even 200.

Thank’s

I didn’t run it on EUR/USD but yes I see it’s been a tough year using Martingale on this pair because of the massive swings.

It’s interesting about the leverage because usually I find the case is the opposite. Please feel free to elaborate on your strategy here or in the forum.

Thanks Steve. great article and website. I have a great affinity with many of the trading strategies described here. I particularly appreciate non-predictive systems which use strong money management. I build EAs and can probably build the martingale for you to share.

I’ve built one that has been running live for about a year and is currently up about 80% after I’ve taken 100% of my captial out. Martingale can work if you tame it. The link is here https://www.myfxbook.com/members/DailyGrind/dailygrindfx/1095746

I’d be interested to work with others on a hedged martingale EA if anyone with some experience to contribute would like to work together. I’ll set up a forum topic to start the discussion.

Always good to hear new ideas:

I’ll pin the link here for anyone who’s interested in working on an EA for this system:

https://forexop.com/boards/thread/lets-build-a-hedged-martingale-ea/

Hey FXGuy, I’d be interested in working together on a hedged martingale EA concept, if you’re still looking to team up.

I’ll check this post regularly, if see you (or anyone else interested) have responded, will leave my contact details.

Great post, Steve!

Thanks

Hi Steve,

Thanks for your sharing..Did you try this strategy using an EA? If yes, how is the outcome?

Regards.

Yes, it’s a proprietary trading advisor, though it doesn’t work on Metatrader. I will get it re-coded to work on MT shortly and make it available on the website. It works well within the parameters above – ie. as a skimmer, but not when over-leveraged. The Excel sheet is a pretty close comparison as far as performance.

I use the martingale system while setting a specific set of rules regarding pip difference at any given moment and a maximum allowable streak of consecutive losses.

Let me explain in detail:

Under normal conditions, the market works like a spring. The more pressure you apply in one way or another at any given moment, there more it wants to rebound in the opposite direction.

For my explanation, I would like to refer to what I call ‘stages’. By ‘stages’, I mean a 10 pip difference upwards (+1 stage) or downwards (-1 stage) from the set price.

For example, if a price is at 1.1840 on a set of currency, and the price moves to 1.1850, I define this as +1 stage. If it becomes 1.1830, I define it as -1 stage.

What I end up doing is choose a given high or low, and wait for it to either rise or fall by 40 pips (rise by 4 stages or fall by 4 stages), and then place a counter-trend order with a set-profit/stop loss of 1 stage in the opposite direction. If I gambled right, I earn. If not, the price keeps going the trend by another stage and I generally lose approximately 2-3x the potential earning due to the spread.

If I win, I just wait for the process to happen again, and place a new order. If I don’t, I double my next bet with a counter-direction stage immediately upon the loss of the 1st stage. In this case, the price has already gone up or down by 5 stages (50 pips), so chances it will at least ease off a bit of pressure by going 1 stage in the opposite direction are increased, and I have higher chances of doubling my original loss.

If I loose again, I double one more time (with even more increased chances I will win the next stage) by taking my first loss + my second loss, and doubling that. If I loose the 3rd stage, I lost a big amount, so I stop doubling there. In that scenario, the market is likely in a run-off one way or the other (generally due to some major event that might cause this to happen to a certain set of currency). I let that set of currency go while looking to re-do my work on another set of currency until the excitement ends (falls by at least a stage or two) on the one I let go.

When looking at a set of currency, I look for sudden rises or falls of 4 stages without ANY counter-direction stage movements in between. If there has been even 1 stage difference, I re-start the stage rise-fall count at 0.

As I said, 90% of the time, I win, and the combined earnings of stages 1, 2 or 3 above the original 4 stage movements generally outweigh the total amount lost over time from those that go over 3 (sudden rises or falls of 70 pips or more without any counter-movements are extremely rare)

I have been using this strategy for about 6 months now, and I am at a positive 35% earning since I began using it. Any thoughts?

Reply on this page: https://forexop.com/boards/thread/discrete-martingale/

Truly thanks Steve for your sharing! I find your sharing is the most precious after reading through many websites covering different aspects of FX.

what if u have a system that cant give u 5 consecutive draw down in a row and i have tested it. so why cant one use martingale strategy.

pls reply

thanks

Thanks for your comment. Please explain a bit further so I can understand what you mean.